To build a successful tax practice, Tax Filings for a Corporations are a must. It will setup your practice from Books to Taxes, everything. Providing Accounting, Bookkeeping, Payroll and Taxation services can be a complete package solution for your clients.

Many a times, students want to study corporation taxes, but they lack understanding of Accounting and Bookkeeping basics, which of course is mandatory.

And if you are ready with that, you can also be ready with tax filing for corporations, which is Income Tax T2.

But, as you take your steps towards Corporation Tax filing, there can be lot of confusion, questions, clarifications and probably you are looking for simplification. The purpose of this guide will be make every simple, right from what is a corporation to is corporation worth it, what do directors, officers or shareholders mean and actually in a corporation with only one person who is what?

It will also cover annual tax filing and minute books.

Let’s Start:

1. What is a Corporation?

- A corporation is a legal entity that is separate and distinct from its owners (referred to as shareholders).

- For this reason, being incorporated can provide small business owners in Canada with the most tax and liability advantages.

- Like individuals (you and me), corporations have many of the same rights and responsibilities.

- For example, corporations can enter contracts, lend and borrow money, sue and be sued, hire employees, invest in assets, and pay taxes (usually at a lower rate).

2. Articles of Incorporation

- A corporation is formed by filing an Articles of Incorporation with the government, which outlines:

-

- corporation’s name

- share structure and any restrictions on share transfers

- corporation’s number of directors

- restrictions you might want to set for your business or business activities

- any other provisions.

-

- The Articles of Incorporation (commonly called “Articles”) is like your corporation’s birth certificate.

3. When Should You Incorporate?

- Regardless of the business structure you start with, as your business grows, the time will come when you’ll want to consider incorporating.

- This usually happens when the business is generating surplus profits and you, as the business owner, have more revenue than you need to cover personal expenses. By incorporating, you can leave surplus profit in the business, allowing you to defer personal taxes on the withdrawals.

Other reasons include:

-

- Incorporate early to reap the benefits

- Incorporate before you sign contracts to enjoy limited liability protection

- Incorporate early to establish business interests among founders

- Incorporate before hiring employees helps to protect your assets

- Incorporate before you add partners or co-owners

4. Incorporation – How to Evaluate?

- Unlike a sole proprietorship or partnership structure, a corporation is its own legal entity that in most cases provides the owners protection from liability.

- This separation between the corporation and its owners means that the personal assets of shareholders are generally protected from business debts and legal obligations, providing them a layer of security. In addition to liability protection, incorporation often brings the advantage of potentially lower tax rates, particularly for small businesses eligible for the small business deduction.

- This tax advantage can translate into substantial savings for shareholders, allowing them to retain more of their earnings for reinvestment or personal use.

- It’s essential to weigh these benefits against the associated costs and complexities of running a corporation. Setting up a corporation typically involves higher administrative costs, including incorporation fees, ongoing compliance requirements, and the need for assistance to navigate complex tax filing obligations.

- These additional expenses and administrative burdens can require a significant investment of both financial resources and time.

- Evaluating your business and personal goals against the costs, both financial and investment of time, can help you decide if this structure fits your needs.

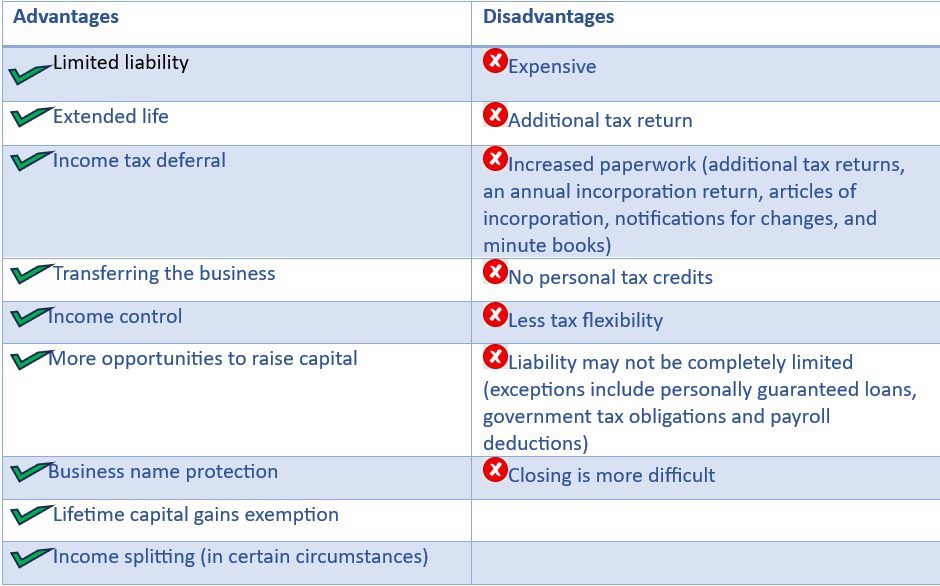

5. Is Incorporation Worth It?

The two biggest benefits of incorporation

- Limited liability to protect personal assets: The most important benefit of incorporation is the protection it provides by limiting the liability of the owners, or what they are responsible for under the law.

- Since a corporation is its own legal entity, it pays taxes, incurs debt and can be even be sued.

- However, in most cases, your personal assets are protected against creditors or if legal action is taken against the business (talk to a tax specialist about exceptions).

- This means that incorporating can help shield you and, by extension, your family from financial harm.

- While the liability of the corporation does not generally extend to you personally, it is important to understand that there are certain situations, such as if a corporation owes GST/payroll amounts to the CRA, where the directors can be held personally responsible for payment.

- Low tax rates: Businesses that operate as sole-proprietorships or partnerships generally pay a higher personal income tax rate on profits as opposed to incorporated business.

-

- For example, if your income hits $250,000, your personal tax rate might average out to 33% federally.

- The federal tax rate for incorporated businesses earning active income is 15% and could be as low as 9%.

- Applicable provincial tax rates would also apply. It’s easy to see that incorporating a business could help save you a significant amount of money in tax

6. Shareholders

- Shareholders are the owners of the corporation.

- Shareholders own shares in the corporation. Like you can hold a “share” or a “piece” of a land, you can hold shares in a corporation.

- The shares give the shareholders the right to vote to make decisions and/or receive dividends, along with many other rights (these two are the main rights).

- Note that shares can be: voting or non-voting (i.e., the shareholders who own shares can vote to make decisions on behalf of the corporation)

- Participating or non-participating(i.e., the shareholders who own shares can receive dividends from the corporation)

- Any person can own shares in a corporation.

- A corporation can own shares of another corporation.

7. Directors and Officers

- Directors are responsible for supervising the corporation’s activities and making decisions regarding those activities.

- Directors of a corporation are not required to hold shares in the corporation.

- A director must:

-

- be at least 18 years old

- not have been declared incapable

- be an individual (a corporation cannot be a director)

- not be bankrupt

-

- Officers are responsible for the day-to-day operation of the corporation.

- Directors and Officers are usually the people who sign off on things like tax returns, loan documents, etc.

- In most situations, the director and officer will be the business owner (shareholder).

8. What does all this mean for small business owners?

- In most cases, you (the small business owner) will likely be the voting shareholder (along with family members like your spouse also owing shares), director, and officer of your corporation.

- But know that you wear different hats for legal purposes:

-

- a shareholder

- director

- officer

-

- So, when you sign off on legal documents or financial statements, you will likely be signing off in your capacity as a director or officer rather than as a shareholder.

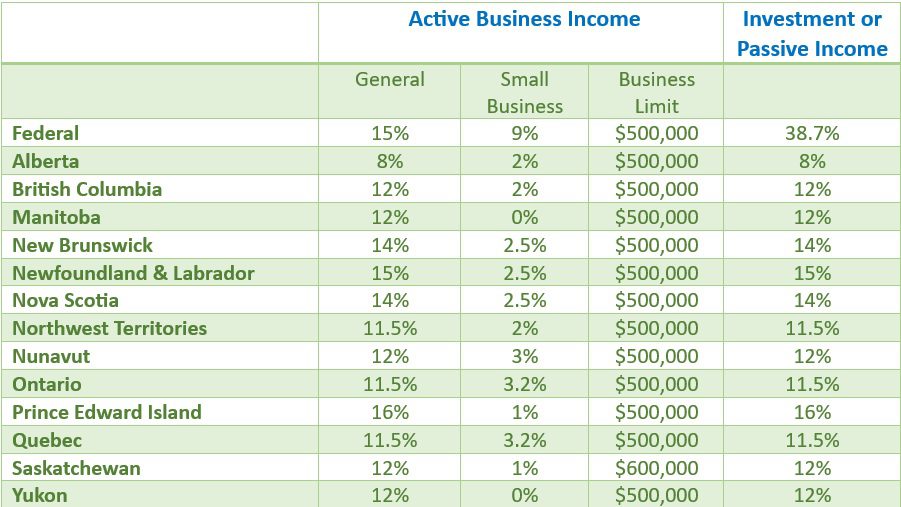

9. 2024 Corporate Income Tax Rates

10. Annual Return filing deadlines

What’s an annual return?

-

- Despite having a similar name, an annual return is different from an annual tax return.

- It is a corporate law requirement that lets Corporations Canada know that your business is “active”—essentially, that you’re still in business.

- Regardless of the size of your corporation, you are obligated to file an annual return if your corporation’s legal status is “active” (that is, not dissolved, discontinued, or amalgamated with another corporation).

- If you do not file or file late, you will not receive a “Certificate of Compliance” from Corporations Canada

What does a Certificate of Compliance do?

-

- A Certificate of Compliance is often needed to support a loan request or to provide assurance to a potential investor that a corporation has not been dissolved

What’s included in an annual return?

-

- Your annual return can be filed online.

- To file you need:

-

- The date of your last annual meeting

- Your type of corporation: private or public

- To be a director, officer or authorized individual who has relevant knowledge of the corporation and is authorized by the directors

-

- Annual return filing deadlines

-

- Every incorporated business must submit an annual return every year to Corporations Canada within 60 days of its anniversary date.

- The anniversary date is the month and day on which the corporation was created or the date on which the corporation first came under the jurisdiction of the Canada Business Corporations Act. You do not need to file for the year the business was incorporated.

-

- To file you need:

- Your annual return can be filed online.

11. Consequences of not filing an annual return

- Corporations Canada has the power to dissolve a corporation that has not filed its annual returns.

- Dissolution can have serious consequences, including not having the legal capacity to conduct business. This includes raising capital or accessing credit and loans.

- While the law allows Corporations Canada to dissolve a corporation after one year of non-filing, the policy is to only dissolve a corporation when it has not filed an annual return for two years.

12. What are minute books?

Minute books are detailed records that document an incorporated company’s structure and activities.

They must be updated every year as part of the incorporation’s annual return to maintain its legal structure and include:

-

-

- Articles of Incorporation

- Articles of amendment

- By-laws

- Resolutions and minutes

- Share certificates and share transfer registers

- Directors, Officers and Shareholder Registers • Notices that have been filed − Change of registered office address − Changes regarding directors • Shareholder agreements They also track key company decisions such as granting of shares, dividends and management fees.

-

Why do they matter?

-

-

- Minute books are required to maintain an incorporation.

- If a business does not have them or keep them up to date, they could be found in default of mandatory government notice filings (making them non-compliant); fined by the CRA as part of an audit; refused for loans by banks;

- and any potential future sale of their business or assets could be in jeopardy or face lengthy and expensive legal delays.

-

Conclusion

Tax courses with certificates from Fintech College offer a valuable pathway to enhance your career. With flexible learning options, comprehensive curriculum, and recognized certification, you can gain the skills and credentials needed to succeed in the competitive field of taxation. Start your journey today with Fintech College and unlock your potential.